ACE 2026 - September 8th

The bimonthly news publication for aviation professionals.

The bimonthly news publication for aviation professionals.

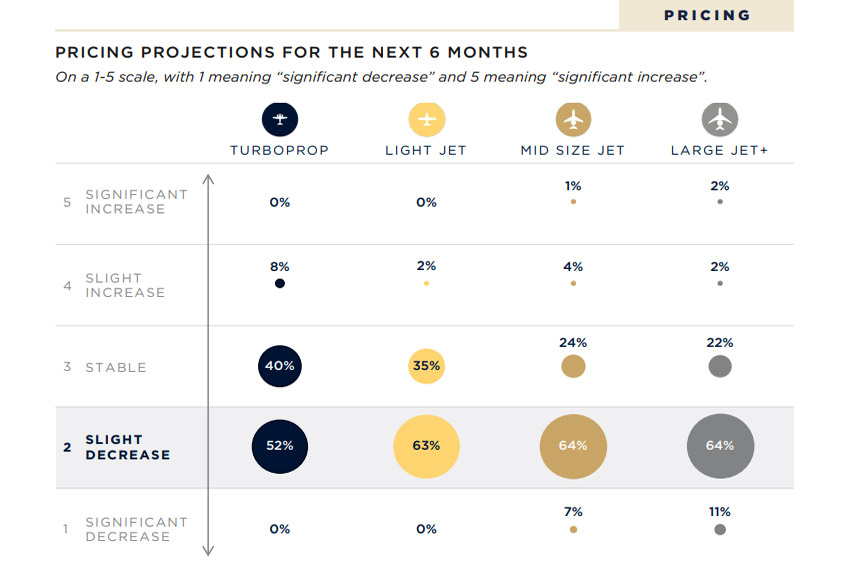

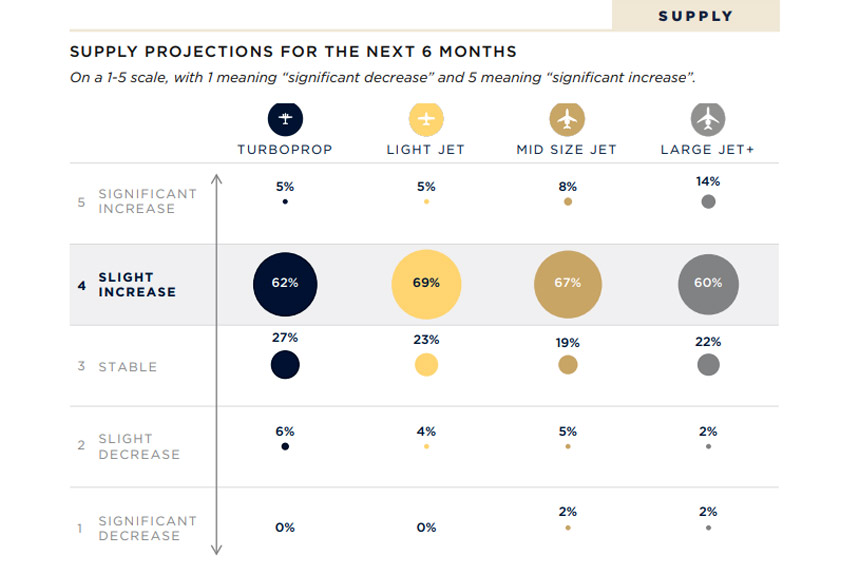

Expectations in the pre-owned business aircraft marketplace for the next six months have increased compared to the outlook in 4Q22 according to the First Quarter 2023 Market Report's global perception survey of IADA members.

Supporting these expectations are first quarter sales results from IADA's accredited dealers, who routinely buy and sell more aircraft by dollar volume than the rest of the world's dealers combined. IADA dealers closed 239 transactions in the first quarter of 2023, compared to 288 deals in the same period in 2022 and 213 in the first quarter of 2021.

IADA dealers ended the first quarter 2023 with 197 aircraft under contract, compared to 259 a year ago and 248 in the first quarter of 2021. Interestingly, 52 of the first quarter 2023 transactions experienced lowered prices while only six did the same period a year ago and 27 in the first quarter of 2021. The full report is available for download from IADA's AircraftExchange website.

Results from the survey suggest that marketplace forces are at work as expected. There has been some replenishment of inventory levels and a return to more rational pricing and valuations amid an environment of continuing customer interest and inquiries.

Even though macroeconomic forces, geopolitical tensions and the latest banking crises flood the headlines, customers appear to be little swayed from their interest in buying, selling and flying business aircraft. While 2023 activity levels of aircraft sales, flight activity and MRO shop demand have generally slipped back from record highs in 2022, the market for business aviation products and services remains vibrant.

“There is evidence that demand and supply forces are rebalancing, with less frenetic activity, more realistic pricing and a slow but steady build up of available inventory,” says IADA chair Zipporah Marmor, vice president of transactions for ACASS in Montreal. “Although specific low-time aircraft with attractive pedigrees continue to attract top dollar, the overall market has begun to downshift from a peak characterised by accelerating prices and strong residual values.”

“Although pre-owned inventory levels have begun to slowly replenish, most OEMs have grown their order backlogs to represent more than two years of production and they are straining to accelerate deliveries in the face of slowly recovering supply chains,” adds IADA executive director Wayne Starling. “Our organisation foresees a continuation of relatively tight market conditions through 2023, driven by customers who cannot or will not wait two or more years to receive their next aircraft.”

IADA began monthly tracking of pre-owned sales metrics for business aircraft in April 2020 as a result of the volatile market conditions caused by the pandemic. Two key factors inform the report: the first is IADA members' market perspective, taken from a survey of the entire IADA membership; the second is actual sales data supplied by IADA accredited dealers to support those points of view.

IADA dealers submit monthly transaction and activity reports and their comments add context to the report:

"Pre-owned buyers are expecting significant price reductions but inventory remains low, especially on late model aircraft," says Robert Sammartino of accredited dealer Skytech in Maryland.

"Surprised by how many acquisitions we have already confirmed for early in 2023. Feel that early part of 2023 will be a bit slower, but latter part of 2023 is looking even more active," says Chad Anderson of accredited dealer Jetcraft in London, UK. "Still low inventory and a seller's market. Buyers being more cautious but still active," adds colleague Todd Spangler.

"I don't expect any large swings in inventory or demand. I believe that the used market will, however, remain strong all throughout this year," says Jeremy Cox of verified products and services member JetValues Jeremy in Illinois.

"Feeding frenzy is over. The market has slowed to a balanced pace, yet with lots of inquiries and activity. Inventory is limited, but not like last year," says Bryon Mobley of accredited dealer Wetzel Aviation in Colorado.

"Certainly a little calmer compared to third and fourth quarters 2022, but we are very steady and keeping busy; normal busy," says Daniel Cheung of verified products and services member Aviation Tax Consultants in Arizona.

"A slight pause in January and February but activity has come back in last couple of weeks," says Joseph Carfagna of accredited dealer Leading Edge Aviation Solutions in New Jersey.

"We are seeing increased balance between buyers and sellers in today's marketplace. This is driven by increased inventory, more realistic pricing and a return to standard transaction dynamics (including pre-buys)," says Emily Deaton of accredited dealer jetAVIVA in Kansas.

"Sellers are still trying to maintain a sellers' market by keeping prices high. However, buyers are refusing to pay these prices. Currently the aircraft sale market is off to a very slow start for the year," says John Swartz of accredited dealer Swartz Aviation Group in Texas.

"If it weren't for supply chain issues limiting OEM production capacity, we'd be looking at a best ever," says Ronald Smith of accredited dealer Western Aircraft in Boise, Idaho.

"The pack has separated. Every market's for itself. Some are firm, others are soft. Some prices are way down, others remain unchanged," says Mike Swartz of accredited dealer Swartz Aviation Group in Fort Worth, Texas.

"What we are seeing right now is a lot of wait and see. Sellers have not caught up yet with the reality of the market, whereas buyers feel that values will still decline," says Zipporah Marmor.

"Some buyers are on hold due to macro-economic uncertainties, and they believe that prices will continue to soften in 2023. Barring a major recession or major equity market correction, I expect prices to continue to trend down," says Frank Janik of accredited dealer Leading Edge Aviation Solutions in New Jersey.